Europe's gas and power concerns have been fading recently, driven by a fortuitous combination of a mild winter and lower demand for energy. This is good news. But the current gas prices are not low and Europe's gas supply remains fragile. Elevated energy prices are a significant contributor to inflation and a large drag on European growth for this year, at least.

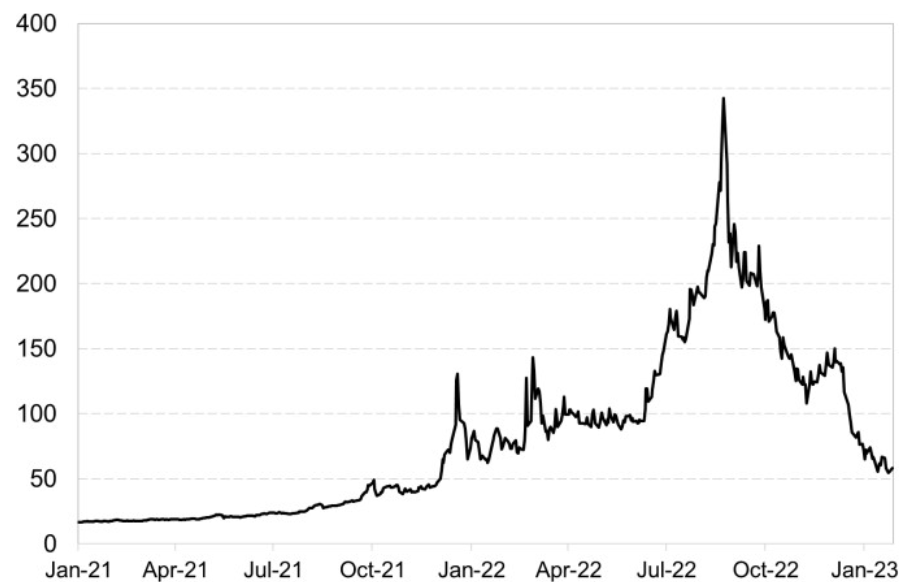

Global gas prices have been on a roller coaster for two years, well before Russia's invasion of Ukraine in February 2022. The European gas price benchmark was about € 17 in January 2021 and went above € 130 in December, to end the year at € 65. Ukraine's invasion in February 2022 pushed the price up a bit, but it is only in July last year that the price reached € 180, before literally exploding in August as it reached € 342. Then gas prices started decreasing and eventually reached the current level of € 55, as shown in Chart 1.

Chart 1: Europe gas prices - TTF natural gas futures (€/MWh).

Source: Bloomberg, mBaer calculations. Dutch Title Transfer Facility (TTF) natural gas futures, in euros per megawatt hours (€/MWh)

Small changes in supply have large effects on gas prices in the EU. Gas is trading in competitive markets and reflects the fragmented structure of the gas supply chain. Since last year prices incorporated EU and single countries' new measures including price caps, subsidies and import bans.

Natural gas markets are fragmented on a global scale. They mainly rely on pipeline infrastructures, which do not allow arbitrage across regions. As Russia shut off the gas supply, Europe looked at liquefied natural gas (LNG) as a primary replacement option, but bottlenecks and congestions at northern European LNG terminals fueled the gas prices' spikes registered last summer.

In turn, these elevated prices suppressed gas demand across Europe (demand destruction). According to Eurostat, the EU gas consumption dropped by about 20% during August- November 2022 compared to the previous five years average. Finally, the 4th warmest winter on record in north-west Europe reduced gas demand for heating purposes and led to the recent

drop in gas prices, currently trading at about € 55. Importantly, high and volatile market prices will eventually encourage a more efficient use of electricity and expanded renewable power. Governments' interventions aimed at reducing levels and volatility of gas prices are not less ineffective than harmful.

Fail to plan, plan to fail

The conflict in Ukraine exposed Europe's dependence on Russia's energy supply. European governments had to step in and take emergency measures to secure alternative sources of energy and prevent high energy prices from damaging their economies. But replacing Russian gas capacity is coming at an exorbitant cost to the taxpayer. These measures are also reshaping the global energy markets' landscape.

Not necessarily in this order, European governments stroke new natural gas deals, committed to new gas infrastructure investments, ramped-up coal usage, enforced voluntary gas demand reduction, introduced a ban on fuel imports from Russia, imposed caps on oil and gas prices and collected windfall profits from energy providers.

Most of the gas shortfall has been replaced by higher imports of LNG and pipeline gas mostly from US, but also from Norway, Qatar, Azerbaijan and North Africa, among others. Europe's success in securing LNG supplies was also enabled by lower demand from China, still under Covid-induced lockdown.

As a result, European gas reserves are currently at around 80% capacity and on track to end the winter over 50% full, based on a simple comparison with the 2020 storage levels.

EU governments also spent or earmarked some € 600bn in subsidies, tax reductions and other fiscal measures to shield consumers and firms from the rising energy costs. Germany alone has earmarked € 264bn. Crucially, the EU Commission estimated that around 70% of these measures are untargeted, as they benefit all or a very large share of the population.

These massive fiscal policy measures are concerning. First, untargeted price measures will lower the price of gas, at a time when Europe needs to reduce consumption and needs to attract LNG suppliers. Second, businesses facing additional uncertainty about gas price levels are likely to delay their investments. Third, governments' largesse may add to further inflation pressures, eventually forcing the ECB to tighten policy even more. Importantly, higher interest rates will inevitably lead to higher debt burdens and lower growth.

The energy crisis is far from over. Europe is on a costly and long path to substituting away from Russian energy. EU measures and market interventions have been successful so far, but risk causing long-term harm to Europe's growth.

Winter may yet be coming.

Francesco Mandalà,

PhD Chief Investment Officer