History is replete with epic changes of heart. Last December, China stunned the world by announcing the exit from the zero-COVID policy, which had been in place since 2020, when Wuhan declared a full-scale lockdown and COVID was known as SARS-CoV-2. Households and businesses no longer should be worried about lockdowns, but the confidence of consumers and entrepreneurs is fragile and sentiment remains shaky. Hardly a surprise after three years of lockdowns.

Chinese government change of mind on the zero-COVID policy has been a show of pragmatism. Mounting economic costs as well as the reduced political incentive to keep the policy in place after the Party Congress in November were the main factors influencing the Chinese authorities sudden decision.

Part of the reason was also the growing evidence against the effectiveness of the zero-COVID policy, as the draconian measures were unable to stop the more infectious viral variant, becoming a reason of rising popular opposition to Mr. Xi's policy.

On the other hand, as the mass testing requirements, the strict lockdowns and the domestic travel restrictions were removed, COVID cases have become significantly underreported, according to the WHO. However, it is rather unlikely that the government may re-enforce COVID restrictions, as the economic cost of reducing infections from the highly transmissible Omicron variant would be prohibitive for the economy.

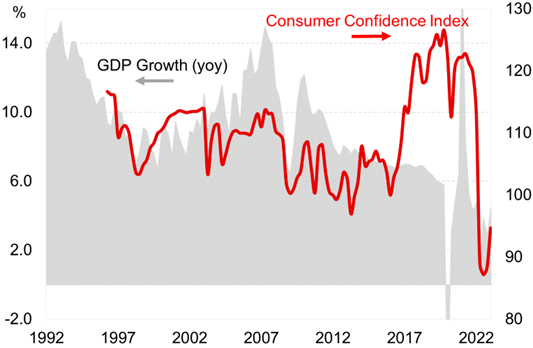

The end of restrictions triggered a recovery, but the jury is out on whether it will ensure consistent progress. In fact, the Chinese economy has slowed significantly in 2022 (see Chart 1) and the slowdown is expected to persist, as the country is facing both cyclical and structural headwinds.

Chart 1: China real GDP growth and Consumer Confidence Index.

Source: Bloomberg, mBaer calculations.

Source: Bloomberg, mBaer calculations.

Economists studying China face tricky theoretical issues.

Liberal economists believe that years of central planning tend to distort prices and misallocate resources, eventually resulting in poor economic performance. Daron Acemoglu, an MIT economist, has no doubt: it is man-made political and economic institutions that underlie economic success - or lack of it.

The more common view is that China would sustain its astonishing growth and will continue outperforming liberal market economies also in terms of innovation.

Take the last four decades as a guidance: China's spectacular economic growth over this period has reshaped the global economic landscape. China became the largest economy in the world in 2016 and its share of the world GDP (in purchasing power parity terms) is now 19%, compared to the US share of just 15%. China has also achieved global leadership as manufacturing workshop, as No.1 trading partner of most nations in the world, as primary engine of global economic growth and as the home to the largest number of the most valuable companies on Fortune's Global 500. These are potent arguments supporting the view that China's growth will continue unabated. Recent data show the economy grew at a fastest pace in a year, as GDP expanded 4.5% in Q1 from a year earlier, beating economists’ expectations and supporting the government's GDP growth target of "about 5%" for 2023 announced at the National's People Congress in March. The government confirmed its pro-growth policy pivot as it increased its budget deficit target, committed to protect the rights of entrepreneurs and introduced various measures to counter the housing slump. Officials' reference to "the need to boost market confidence" and to "the rights and interests of entrepreneurs" are welcome shifts in the Party's rhetoric.

Red flags flutter in the headwinds

China's prospects today look far less rosy than they did in the good old days of double-digit GDP growth (see Chart 1).

First, the economy has been experiencing a structural slowdown over the last decade. The evergreen list of structural economic headwinds (ask any economist at the IMF) comprises chronic over-investment, misallocation of capital - real estate, one for all, weak productivity growth, worsening public finances, population aging and tightening central control on the economy.

Second, the pandemic has slowed China's growth outlook, as confidence and sentiment of consumers and business plunged.

Third, the real estate market slumped badly over the last two years since the collapse of Evergrande, a large real estate developer, and the property sector is still going through a sharp contraction. The backlog of partially built housing is at risk of non-completion, resulting in further weakening of households' confidence. Fourth, and importantly, the external environment has deteriorated, with increasing recession risks in US and Europe, resulting in lower global demand for Chinese exports. The growing US-China rivalry and distrust, as shown by the spy balloon incident, is an additional headwind for China economy as America is ramping up sanctions and tariffs on Chinese exports.

Our view: The recent rebound of the economy may suggest the most difficult period has passed. Yet, China faces significant economic challenges, and it will take time to recover from the zero-COVID policy. China's growth trajectory looks unpromising.

Francesco Mandalà, PhD Chief Investment Officer