Crude elections: will oil be the silver bullet for Democrats in 2022?

When Edwin Drake invented the technology to extract crude oil in Pennsylvania in 1859, he created an extremely valuable commodity. Little he knew he would even appear one century later in the comics series Lucky Luke, in the episode "In the Shadow of the Oil Rigs".

Since Drake's discovery, oil fueled cars, home heating, economies, wars and geopolitics. For economists, changes in oil prices are the paradigm of a global shock, an event likely to affect many economies at the same time. In fact, substantial increases in the price of oil (oil shocks, in jargon), led to economic recessions, resulting in permanent losses in jobs and welfare, eventually determining the political fortunes of democratic governments and totalitarian regimes.

Two of the major episodes of economic recession and high inflation in most industrialized economies were caused by huge increases in the oil price, triggered by the OPEC embargo and the Iranian revolution in the mid and late 1970s.

Anecdotal evidence suggests that voters' behavior is equally influenced by ideology as well as by oil and gasoline prices.

A recent study on the link between oil prices and election results concluded that an increase in oil price ahead of the polls reduces the likelihood of re-election for the incumbent party.

Both right-leaning and left-leaning incumbent parties are likely to lose elections following a crude oil price increase, according to this study. And, as oil and gas prices rose sharply since the beginning of the year, some Republicans named President Biden "Jimmy Carter 2.0", as President Carter lost the 1980 elections against Ronald Reagan at the same time as gasoline price reached its peak.

Oil prices at the millennium

The 2000s are different from the 1970s and the 1980s, though.

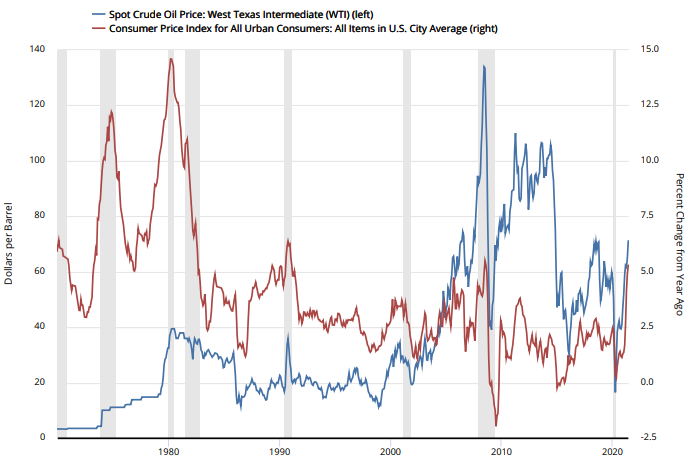

The reason is that, since the 1990s, the global economy has experienced two oil shocks of magnitude comparable to those of the 1970s but, in both cases, developed economies and inflation remained relatively stable in response to elevated oil prices. Chart 1 clearly shows that oil prices increases before the 1990s led to two-digit inflation and deep economic recessions in the US. After the 1990s, oil price increases did not translate in higher inflation, and also the two most recent US recessions are rooted in the great financial crisis and the Covid-related shutdown, respectively.

A famous study confirms this observation, as the authors conclude that the most recent surges in oil prices had only mild effects on inflation and economy activity because of "[…] good luck, smaller share of oil in production, more flexible labor markets, and improvements in monetary policy". By "good luck", the authors mean lack of additional negative economic events. The other features identified in the study are related to the structural and institutional changes in the US economy including weakening unions, increasing competition and declining minimum wages. This means that as workers in the 1970s faced sharp inflation increases they obtained a rise in nominal wages, which then led to further higher prices, whereas in the 2000s nominal wages did not increase following inflation rises.

Importantly, in the 2000s, the US Federal Reserve (Fed) has cemented its credibility in keeping inflation under control therefore avoiding the use of higher interest rates to bring down inflation. By contrast, in 1980-82, Fed Chair Paul Volcker solved the problem of high inflation by dramatically rising interest rates causing a significant double-dip recession.

Chart 1: Oil price, inflation and US recessions

Shaded areas indicate US recessions. Source: US Federal Reserve Bank.

A lot of the inflation seen so far this year can be attributed to the trillions of liquidity injected in the economy by central banks and governments, by labor shortages in certain sectors and bottlenecks in the global supply chains. Oil prices raised strongly but there is no evidence that higher prices pushed inflation higher so far this year. A large part of the inflation this year is also due to consumers and producers' expectation that inflation may go higher because, as we wrote in our February issue (Is this the end of central banks’ independence?), the Fed and the ECB are losing their independence in conducting their monetary policy.

We believe that the Fed is at a turning point and will announce already in Autumn a reduction of its bond-buying program and signaling future interest rate hikes, as inflation will remain well-above the 2% target, potentially slowing down the economy.

As we are entering a new testing period with high inflation, the monetary policy will have a larger influence than oil prices on the result of the midterm elections.

Francesco Mandalà, PhD

Chief Investment Officer

Disclaimer

This document is for information purposes only. It constitutes neither an offer nor a recommendation to purchase, hold or sell financial instruments or banking services, and does not release the recipient from carrying out their own assessment. The recipient is recommended in particular to check the information in terms of its compatibility with their own circumstances and its legal, regulatory, tax and other consequences, possibly on the advice of a consultant. The data and information contained in this publication were prepared by MBaer Merchant Bank AG with the utmost care. However, MBaer Merchant Bank AG does not assume any liability for the correctness, completeness, reliability or topicality, or any liability for losses resulting from the use of this information. This document may not be reproduced in whole or in part without the written permission of MBaer Merchant Bank AG.

Dieses Dokument dient ausschliesslich Informationszwecken. Es stellt weder ein Angebot, noch eine Empfehlung zum Erwerb, Halten oder Verkauf von Finanzinstrumenten oder Bankdienstleistungen dar und entbindet den Empfänger nicht von seiner eigenen Beurteilung. Insbesondere ist dem Empfänger empfohlen, allenfalls unter Beizug eines Beraters, die Informationen in Bezug auf die Vereinbarkeit mit seinen eigenen Verhältnissen, auf juristische, regulatorische, steuerliche, u.a. Konsequenzen zu prüfen. Die in der vorliegenden Publikation enthaltenen Daten und Informationen wurden von der MBaer Merchant Bank AG unter grösster Sorgfalt zusammengestellt. Die MBaer Merchant Bank AG übernimmt jedoch keine Gewähr für deren Korrektheit, Vollständigkeit, Zuverlässigkeit und Aktualität und keine Haftung für Verluste, die aus der Verwendung dieser Informationen entstehen. Dieses Dokument darf weder ganz oder teilweise, ohne die schriftliche Genehmigung der MBaer Merchant Bank AG reproduziert werden.