The road to El Dorado: how housing became unaffordable

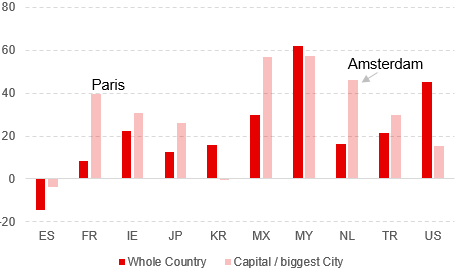

In the 16th and 17th centuries, the myth of El Dorado, a lost city of gold, led many Spanish conquistadores on a fruitless trek into the rainforests of South America. These days, the descendants of Hernán Cortés or Francisco Pizarro could just travel to Paris and Amsterdam, as house prices went through the roof, virtually turning bricks into gold bars (see chart below).

Real residential property prices (cumulative changes since 2010, %)

Source: BIS (Aug-21), "Residential property price statistics, Q1 2021".

Cities are places of consumption as well as places of production. Both anecdotal evidence and economic research suggest that bigger cities attract more skilled workers, and more skilled urbanites have experienced greater wage growth. Therefore, the increase in housing prices in big cities certainly reflects both demands from highly paid skilled workers and limits on housing supply. But this is only part of the story.

Red-hot shelter

In many countries, house prices rose steadily after the 2008 recession, driven by low-interest rates and quantitative easing (QE) and even accelerated due to governments and central banks' extraordinary economic support in the Covid crisis.

In the US, the year-on-year reading of the S&P Case-Shiller house price index accelerated to an all-time high of +19.1% in June, and the median price of US homes sold was 16% higher than a year ago in the second quarter. It is a huge increase.

This is a reason of concern for policymakers, as they are currently pondering the unwinding of the support measures. As a consequence, borrowing costs may rise, hence exposing the vulnerability of the real estate sector.

Mr Fritz Zurbrügg, Vice Chairman of the Swiss National Bank (SNB), recently stated: "[…] we consider the vulnerabilities on the mortgage and real estate markets to be at a high level at present". This is as far as a central banker can go in raising a red flag for the Swiss housing market. Memories of the Swiss real estate crash in the early 1990s are still vivid at the SNB.

It is well known that real estate markets are subject to dramatic price fluctuations, which are as hard to explain as are stock or bond price movements. Predicting the future of real estate prices or spotting housing market bubbles remains a job suitable for scholars of the calibre of Nobel-laureate Bob Shiller, who correctly predicted the US housing crash of 2008.

Waking up from the housing dream

We can at least establish that houses look overvalued, as prices have risen to historically high levels across countries and above the levels suggested by fundamental factors, including housing affordability. This is a deceptively simple concept, comprising a mixture of variables including house prices and quality, interest rates and income. Just looking at the US, for example, as similar considerations apply to most developed economies, the year-on-year compensation growth has remained in the range of 2-3%, at least for the last five years, far below the housing price increase the same period.

This implies that housing affordability, simply measured as house price-to-income ratio, has worsened in the US and worldwide, despite low rates. Overall, the surge in house prices together with modest income increase has wiped away the gains in affordability brought by low rates, driven by central banks' near-zero or even negative rates and QE measures.

It means for typical families or young individuals to hold the project to buy a house for now. This is worrying. It is even more worrying that homebuyers may want to buy a house too expensive for them with the expectation that the price will rise even further. Or that house prices are unlikely to fall. The perceived risk of an investment in a house may be too low.

Happy renting? Not for everybody

The common rule that rentalhousing costs should not exceed 30 per cent of household income is a widely used metric for assessing rental affordability. A recent IMF study finds that in many European countries, rental housing has become unaffordable for low-income renters, the young, and those living in cities, as they spend at least 40 per cent of their income on rents. The pandemic has even worsened the affordability of rental housing in Europe and other developed economies, especially in the biggest cities.

A booming housing market creates its discontents. Overpriced houses and expensive rents are causing unease also among governments and central banks. The current levels of house prices and the sharp acceleration registered after the pandemic may prove unsustainable. The cost of inaction may be a severe housing market correction in the upcoming quarters.

Francesco Mandalà, PhD

Chief Investment Officer

Disclaimer

This document is for information purposes only. It constitutes neither an offer nor a recommendation to purchase, hold or sell financial instruments or banking services, and does not release the recipient from carrying out their own assessment. The recipient is recommended in particular to check the information in terms of its compatibility with their own circumstances and its legal, regulatory, tax and other consequences, possibly on the advice of a consultant. The data and information contained in this publication were prepared by MBaer Merchant Bank AG with the utmost care. However, MBaer Merchant Bank AG does not assume any liability for the correctness, completeness, reliability or topicality, or any liability for losses resulting from the use of this information. This document may not be reproduced in whole or in part without the written permission of MBaer Merchant Bank AG.

Dieses Dokument dient ausschliesslich Informationszwecken. Es stellt weder ein Angebot, noch eine Empfehlung zum Erwerb, Halten oder Verkauf von Finanzinstrumenten oder Bankdienstleistungen dar und entbindet den Empfänger nicht von seiner eigenen Beurteilung. Insbesondere ist dem Empfänger empfohlen, allenfalls unter Beizug eines Beraters, die Informationen in Bezug auf die Vereinbarkeit mit seinen eigenen Verhältnissen, auf juristische, regulatorische, steuerliche, u.a. Konsequenzen zu prüfen. Die in der vorliegenden Publikation enthaltenen Daten und Informationen wurden von der MBaer Merchant Bank AG unter grösster Sorgfalt zusammengestellt. Die MBaer Merchant Bank AG übernimmt jedoch keine Gewähr für deren Korrektheit, Vollständigkeit, Zuverlässigkeit und Aktualität und keine Haftung für Verluste, die aus der Verwendung dieser Informationen entstehen. Dieses Dokument darf weder ganz oder teilweise, ohne die schriftliche Genehmigung der MBaer Merchant Bank AG reproduziert werden.